The cost of living crisis is probably on most people’s minds at the moment. What impact does inflation have on annual shared ownership rent reviews? And should shared owners be concerned about RPI?

This is the first of a 2-part feature on shared ownership rent. In Part 1 we’ll cover:

- How shared ownership initial rent is calculated

- Shared ownership annual rent reviews

- How RPI affects annual rent increases

In Part 2 we’ll cover:

- How the amount of shares still held by the landlord affects ongoing rent affordability

- Whether shared ownership is cheaper than the private rental sector (PRS)

- Whether shared ownership is cheaper than buying outright

- The relationship between wages and annual rent reviews

- Your options if you’re not happy with your rent review

On 22 October 2023, the Government published new rent reforms for shared ownership. The reforms aren’t retrospective so the information in this 2-part feature continues to apply, unless a lease specifies the new rent arrangements.

How is shared ownership initial rent calculated?

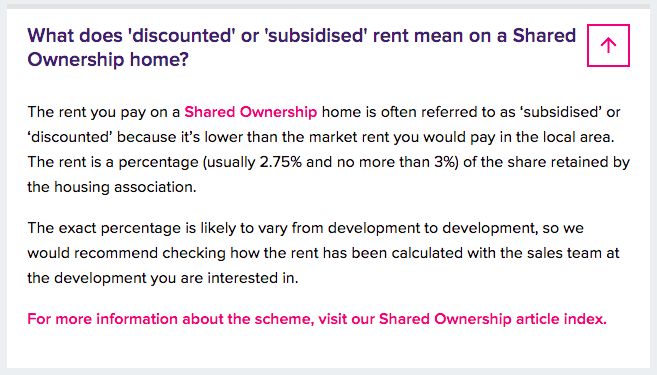

The Share to Buy website explains that shared ownership rent should – initially – be lower than people might otherwise pay in the private rental sector for a similar property.

Say you purchase a 45% share in a shared ownership home with a total value of £300,000. Your share would have a value of £135,000 (£300,000 x 45%), and your housing association’s share would have a value of £165,000 (£300,000 x 55%).

You pay rent to your housing association on their 55% share. If your lease specifies initial rent at 2.75%, then you would pay your housing association £378.13 monthly (£165,000 x 2.75% divided by 12).

But rent doesn’t stay at the same level after the first year.

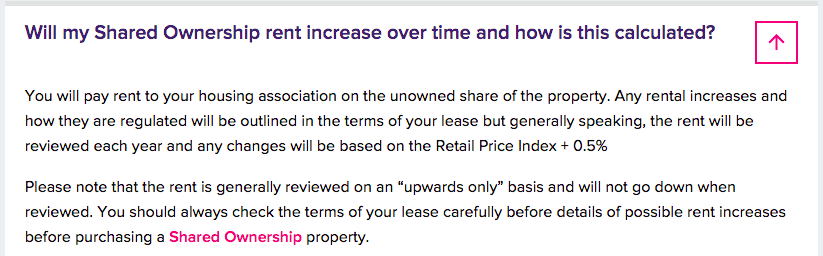

Annual rent reviews

As the Share to Buy website explains – in the Box below – shared owners should expect their rent to increase every year.

There are two aspects to consider:

- Annual rent increases are driven by the Retail Price Index (RPI).

- Shared ownership rent reviews are on an ‘upward only’ basis.

The suggestion by Share to Buy to check your lease contract is good advice. Housing associations will probably say the same.

But Orbit Housing Association’s question – in the Box above – How do you decide to either increase or decrease the shared ownership rent, and by how much? is more than a little disingenuous. Shared ownership rents don’t decrease. Or, at least, rents on shared ownership homes delivered via the Government’s Affordable Homes Programme (AHP) don’t decrease, per the terms of the model lease.

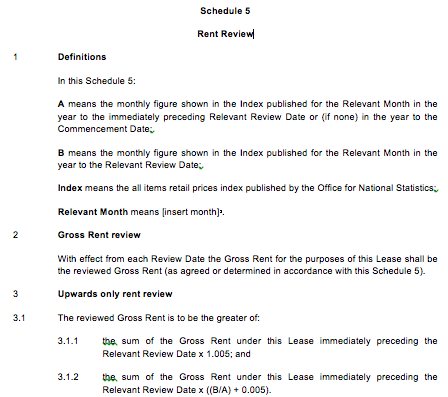

Your lease: what does it say about annual rent review?

Here is a typical Rent Review schedule for a shared ownership flat. It may appear complicated but don’t worry – we’ll go through it step by step.

The key thing to understand here is that rent will either increase by a minimum of 0.5% (shown by the ‘rent x 1.005’ formula at 3.1.1), or RPI plus 0.5% (shown by the ‘rent x RPI change + 0.5%’ formula at 3.1.2) if it is greater.

‘Upwards only rent review’ means that shared ownership rent never goes down, even if RPI goes down.

(There are similar terms for houses, and for homes delivered via previous AHPs. Though older leases may have slightly different terms; perhaps RPI plus 2%).

RPI

What is RPI? RPI is short for Retail Price Index, and it’s a way of measuring inflation by looking at whether prices are increasing or decreasing. As a general rule RPI increases each and every year. (Though RPI did go down in 2009; for the first time since 1960).

One of the problems with using RPI to calculate shared ownership rent increases is that it’s impossible to predict how high RPI might rise in the future. Which means it’s problematic to simply assume that shared ownership ‘will be affordable’ over the long-term.

Additionally, the Office for National Statistics (ONS) say:

They add:

In fact, social housing rent rises are calculated using the Consumer Prices Index (CPI). So, why is RPI used for shared ownership rent reviews? It’s not clear. (A cynic might wonder if it’s because RPI tends to be higher than CPI, meaning that shared ownership rent increases based on RPI generate more rental income for housing associations….? Which, in turn, is used to help cross-subsidise the cost of social rental homes).

RPI plus up to 0.5%

Homes England say:

‘Annual rent increases are to be limited to the Retail Price Index (RPI) plus 0.5%’.

Homes England, Capital Funding Guide, Section 4.2.2

The key thing to note here is that if shared ownership rent increases are ‘limited’ to a level higher than RPI they are, in fact, still rising slightly faster than RPI. Lets look at a couple of examples.

RPI at 1% (rent rise 1.5%)

- If RPI is 1% at the time of an annual shared ownership rent review, then rent will increase by 1.5% (1% plus 0.5%).

- Say rent was £200 per month, it would increase to £203 per month.

- If rent was £400 per month, it would increase to £406.

- If rent was £600 per month it would increase to £609.

RPI at 10% (rent rise 10.5%)

- If RPI is 10% at the time of an annual rent review, then the rent increase will be 10.5% (10% plus 0.5%).

- Say rent was £200 per month, it would increase to £221 per month.

- If rent was £400 per month, it would increase to £442.

- If rent was £600 per month it would increase to £663.

You probably get the picture: high RPI is bad news for shared owners!

‘Upwards only’ annual rent reviews

But looking at shared ownership rent review over a one-year period can underestimate the cumulative impact of annual rent increases. If RPI is high in any particular year (or over a number of years) a compounding ‘upwards only’ rent review policy could start to have a significant impact on affordability.

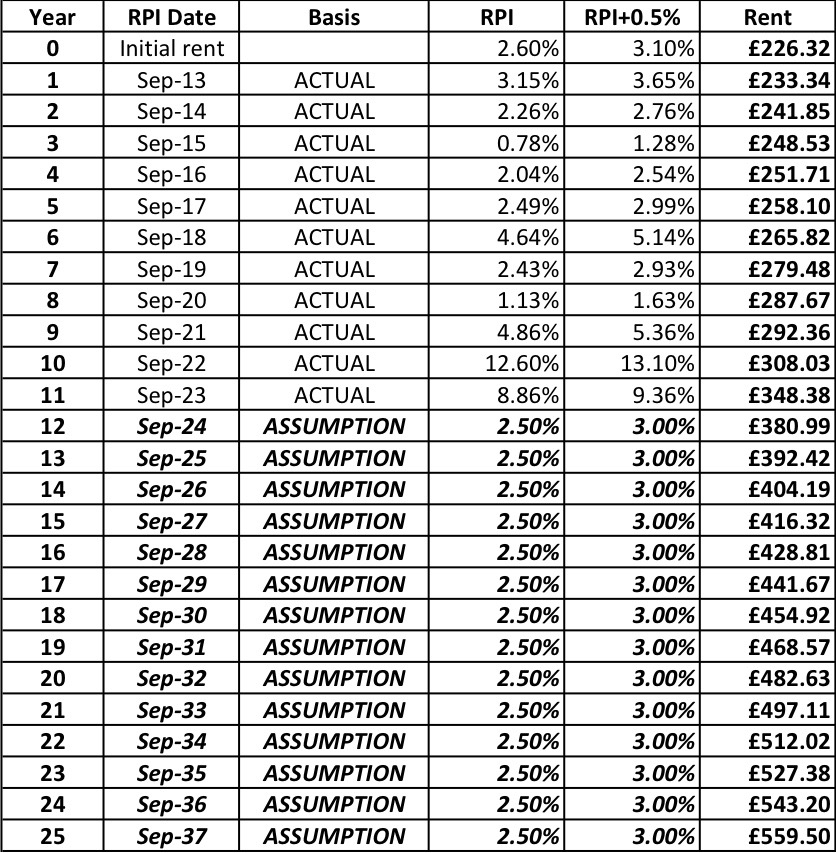

Annual rent review – Example 1

In 2012 Chloe buys a 45% share in a shared ownership home with a total value of £179,563 (the average property price in England that year).

Her initial rent is £226.32 per month (£179,563 x 2.75% x 55% divided by 12). Each year her rent goes up by RPI plus 0.5%. Between 2013 and 2023 Chloe’s rent goes up by £122.06.

Nobody knows what the future will bring! But for this illustration we’ve assumed RPI stays at 2.5% from 2024 until the end of her 25-year mortgage term on her initial tranche. If that were to happen, assuming Chloe doesn’t staircase (buy more shares) her monthly rent would increase from £226.32 in 2012 to £559.50 in 2037.

In practice, RPI would inevitably vary from year to year. It might stay under 2.5% throughout Chloe’s mortgage term. It could be higher than 2.5% in some years and lower in others. It’s impossible to predict. But using an assumption of 2.5% every year makes it easier to see what’s happening in this illustration.

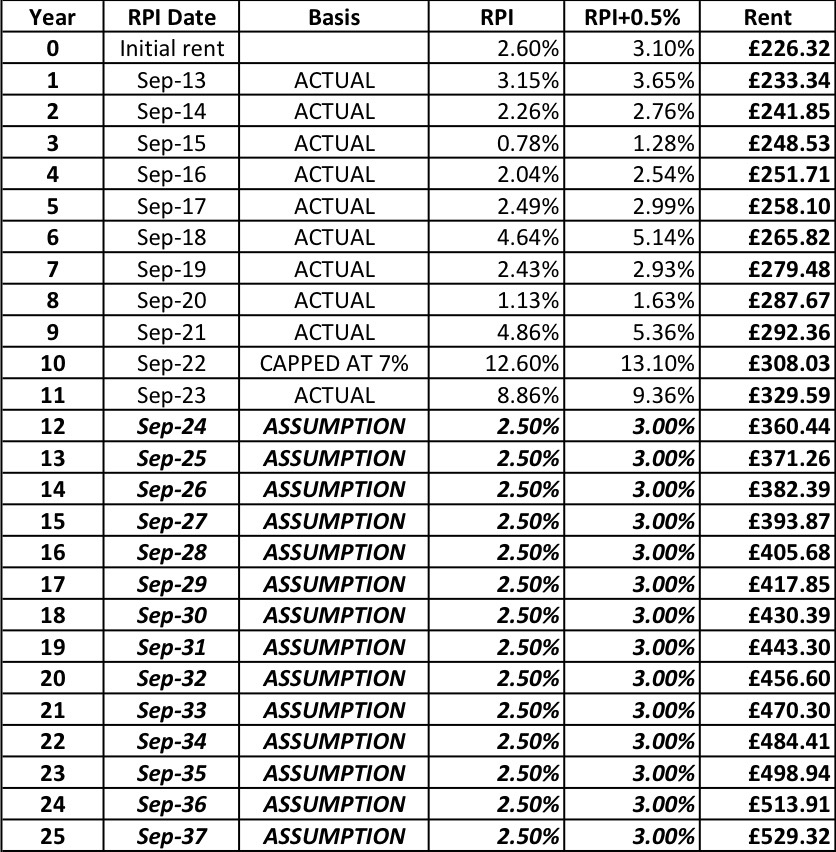

Of course, RPI has risen sharply in recent years. Consequently, many housing associations (although not all) applied a rent cap of 7% in 2023-24.

Annual rent review – Example 2

In Example 2 everything is the same except that Chloe’s housing association applied the 7% rent cap in 2023-24. Between 2013 and 2023 Chloe’s rent goes up by £103.27.

Chloe’s initial rent starts at £226.32 per month (£179,563 x 2.75% x 55% divided by 12) as previously. But this time, again assuming Chloe doesn’t staircase, her monthly rent rises to £529.32 by the end of her mortgage term.

In Part 2 of this 2-part feature we’ll go on to look at other factors affecting the ongoing affordability of shared ownership rent, and whether claims that shared ownership is cheaper than renting privately stack up.

SHAC (Social Housing Action Network) is currently campaigning against unaffordable rent increases for social rental tenants and shared owners. Click here for more information.

UPDATED 26 OCTOBER 2023 – illustrations amended to show effect of reported RPI to 2023, and the 7% rent cap.

Cover image: www.freepik.com

Be First to Comment