Housing Ombudsman ruling on Housing 21 OPSO Extra Care complaint raises questions about discrepancies between Home’s England’s Capital Funding Guide and the housing provider’s evidence.

To: Richard Blakeway, Housing Ombudsman

Date: 8 June 2026

Re: Case ID 202426905, Housing 21

Shared Ownership Resources recently launched a new resource: SO Hub: Buyback policies. The SO Hub signposts visitors to housing associations’ buyback policy (if one exists). Likewise, the hub signposts to Housing Ombudsman rulings on shared owners’ buyback complaints.

In compiling the new SO Hub we were surprised to find a seeming discrepancy between Homes England’s Shared Ownership Capital Funding Guide and evidence provided to the Housing Ombudsman Service by Housing 21, referencing that guidance.

Buyback policy and practice are, of course, entirely discretionary. However, in this case, the discrepancy appears to have had significant financial consequences for the former shared owner who made a complaint to the Housing Ombudsman.

We explain our concerns in more detail below.

The former shared owner’s complaint

On 29 December 2023, Housing 21’s Home Ownership Manager emailed the shared owner to confirm that buyback would be offered at 80% of the purchase price. Following this the Head of Extra Care sent a message to the resident saying that buyback would be at 80% of the market price, not the purchase price. Then, in a follow up email to the resident on 15 January 2024, the landlord’s Head of Extra Care said they were “incredibly sorry” for their “error” in offering 80% of the market price.

The former shared owner made a formal complaint to Housing 21 on the basis she had been told she would be offered 80% of the current market price.

Housing 21’s response

In evidence to the Housing Ombudsman Service investigation, Housing 21 claimed that – under Homes England’s Capital Funding Guide – the landlord could only offer 80% of the purchase or market value of the property, whichever was the lower.

Homes England’s Capital Funding Guide

A quick check by the Housing Ombudsman Service would have demonstrated that Homes England’s guidance is not as claimed by Housing 21. Nowhere does the guidance state that providers must offer: “80% of the purchase or market value of the property, whichever was the lower”.

Rather, guidance refers to an ‘open market valuation carried out by an independent RICS qualified valuer, which supports the amount paid to repurchase the property’.

We contacted Homes England to query Housing 21’s evidence to the Housing Ombudsman Service. They confirmed our understanding that ‘open market valuation’ refers to the current market value and not the original purchase price.

6.3.2 Equity repurchase

Similar to downward staircasing there is no ‘right’ to equity repurchase with any decision being at the provider’s own discretion. For example, to support their asset management strategy.

However, due to the role of equity repurchase in also addressing the challenges associated with building safety, providers should make details of any policies related to the repurchase of a shared owner’s equity available on their websites in a clear and accessible format. Even if it is to make clear that they do not operate such a policy.

Recycled grant can be used to fund up to 100% of the equity repurchase costs. Providers should ensure they retain any documentary evidence of their decision to use recycled grant to fund equity repurchase. This includes the open market valuation carried out by an independent RICs qualified valuer, which supports the amount paid to repurchase the property.

Handling of the complaint

The Housing Ombudsman’s report on the case concluded that: ‘The landlord provided a reasonable response to the resident’s concerns’. A conclusion which was based on the following statements: ‘In 2015 the landlord’s board approved a proposal to offer to buy back properties at 80% of the ‘initial investment’ (purchase price). This was confirmed in an executive team meeting in October 2023 where its draft Buy Back Policy and Procedure was agreed’.

But this completely overlooks the fact that Housing 21’s draft Buy Back Policy and Procedure appears to be based on a fallacy. Assuming, of course, that the Buy Back Policy and Procedure is governed by Homes England’s guidance, as is implied in their evidence to the Housing Ombudsman.

“When offering to buy back a property we can only offer a value of 80% of the purchase price or market value, whichever is lower. We are governed by Homes England Capital Funding Guidance because they funded the construction of the property in the first place.”

All in all, it is hard to understand why the Housing Ombudsman Service found no malpractice and no additional learning.

Compliance with the Capital Funding Guide: transparency

Housing 21 fails to comply with the Capital Funding Guide in another important respect. Homes England’s guidance states that: ‘Providers should make details of any policies related to the repurchase of a shared owner’s equity available on their websites in a clear and accessible format. Even if it is to make clear that they do not operate such a policy’.

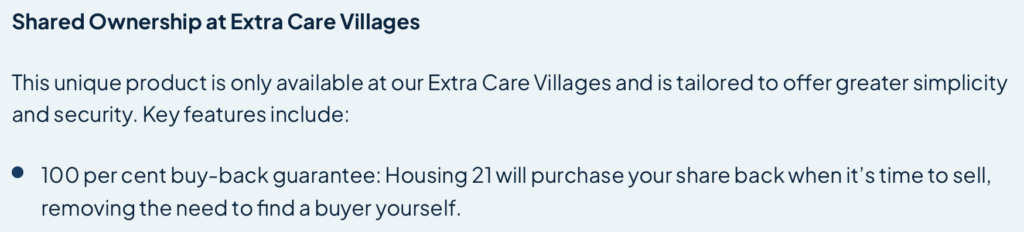

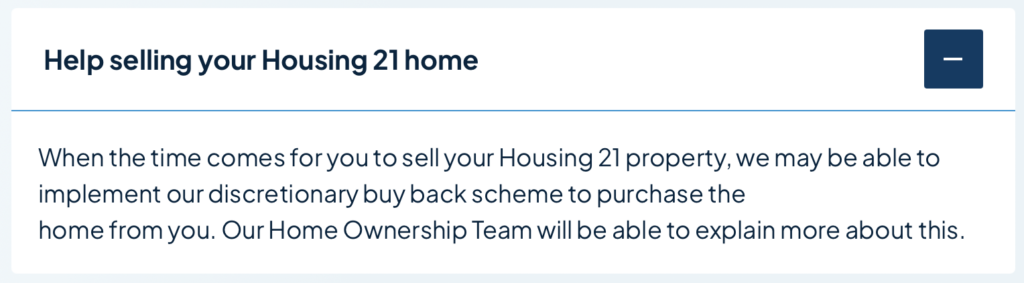

Yet Housing 21 still doesn’t include their buyback policy in the A-Z list of policies published on their website. Rather, they promote a “100 per cent buy-back guarantee” and a “discretionary buyback scheme”. Neither of which provide the vital information that would enable people to make informed transactional decisions.

Questions arising for Housing 21 and for the Housing Ombudsman

Housing 21

This case raises some questions about Housing 21’s internal management and governance. Is the Buy Back Policy and Procedure based on Homes England’s guidance, or not? If it is, why diverge from that guidance? And, if not, why make reference to being “governed by Homes England Capital Funding Guidance” in evidence to the Housing Ombudsman Service?

Housing Ombudsman Service

Shared owners often get a poor deal. As the National Audit Office concluded in a 2026 report on shared ownership, long term financial risks aren’t always understood.

It is therefore vital that Housing Ombudsman Service investigators are adequately trained and resourced to deal with shared owners’ complaints, including buyback. Yet this case raises questions about alignment of Homes England’s guidance and the Housing Ombudsman Service regarding complaints from shared owners, at least when it comes to buyback.

We look forward to your response.

Be First to Comment